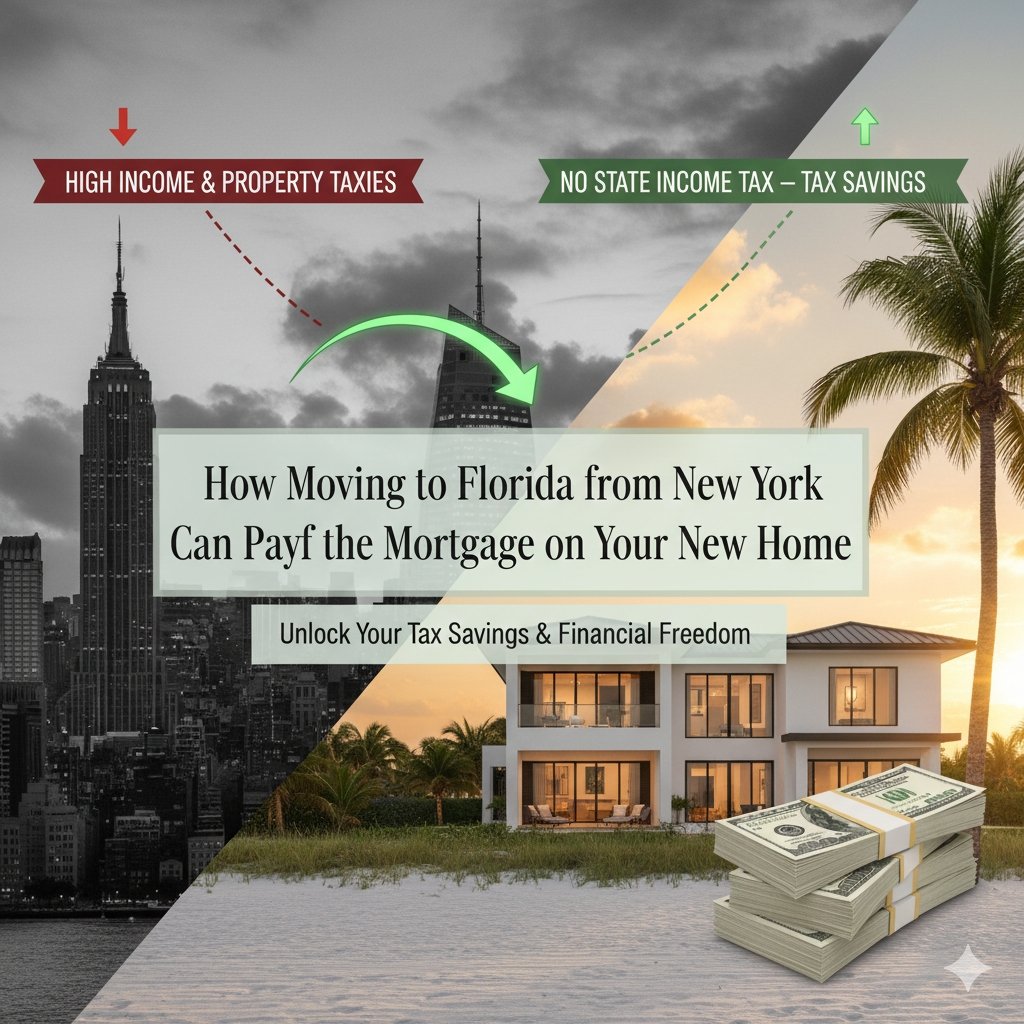

How Moving to Florida from New York Can Pay for the Mortgage on Your New Home

For high-income professionals earning between $500,000 and $2 million annually, moving to Florida represents more than a lifestyle change. It’s a financial transformation that can fund the purchase of a substantial Miami property through tax savings alone.

The mathematics are compelling. New York State and New York City together impose some of the highest combined income tax burdens in the nation. Meanwhile, Florida maintains zero state income tax and zero local income tax. For six-figure earners, this differential doesn’t just represent abstract savings—it translates directly into mortgage-buying power.

This article examines three real-world income scenarios, calculating precisely how much each earner saves by moving to Florida and determining what that means in concrete real estate terms. The results demonstrate that for many high earners, their annual tax savings can genuinely cover—or substantially offset—the mortgage payment on a Florida home.

Table of Contents

- 1. Introduction: The Florida Tax Advantage

- 2. Understanding the New York Tax Burden

- 3. The Florida Zero-Tax Reality

- 4. Scenario 1: $500,000 Income Earner

- 5. Scenario 2: $1 Million Income Earner

- 6. Scenario 3: $2 Million Income Earner

- 7. Complete Tax Savings Comparison

- 8. Miami Neighborhoods That Match Your Budget

- 9. Establishing Florida Residency the Right Way

- 10. Property Taxes: New York vs. Florida

- 11. People Also Ask

- 12. Conclusion: Your Path Forward

Understanding the New York Tax Burden

Living and working in New York City subjects residents to a double layer of income taxation that distinguishes it from nearly every other metropolitan area in America.

New York State imposes a progressive income tax with rates climbing to 10.9% on income exceeding approximately $25 million for married filers. However, most high earners face effective rates in the 6-9% range once deductions and the progressive structure are factored in.

New York City adds its own separate income tax, with rates ranging from 3.078% to 3.876% depending on income level and filing status. Unlike state taxes that affect all New York residents, this city tax applies exclusively to those living within the five boroughs.

When combined, these two tax systems create a substantial burden. A professional earning $1 million annually might assume their effective combined rate is simply the top marginal rates added together, but the reality involves a complex calculation across multiple brackets.

For this analysis, we’re using realistic effective tax rates—the actual percentage paid after accounting for the progressive structure:

- $500,000 income: 9.5% effective rate

- $1,000,000 income: 11.5% effective rate

- $2,000,000 income: 13.5% effective rate

These represent the combined New York State and New York City burden, excluding federal taxes which remain constant regardless of where you live.

The Florida Zero-Tax Reality

Florida’s tax structure stands in stark contrast to New York’s multi-layered approach. The state constitution explicitly prohibits a personal income tax, a provision that has remained intact for decades and enjoys strong political support across the spectrum.

This means Florida residents pay:

- 0% state income tax

- 0% local income tax

- 0% city income tax

Your entire state and local tax obligation disappears the moment you establish legitimate Florida residency. Federal income taxes remain unchanged—whether you live in Manhattan or Miami, the IRS still expects the same payment. However, the elimination of state and local taxes creates immediate, substantial savings.

For high earners, this differential becomes transformative. While someone earning $75,000 annually might save $7,000 by moving to Florida—a meaningful amount—someone earning $1 million saves more than $110,000. At $2 million in income, the annual savings approach $270,000.

Ready to Calculate Your Savings?

Contact me today for a personalized analysis of how moving to Florida could impact your finances and real estate goals.

Scenario 1: The $500,000 Income Earner

Let’s examine our first hypothetical professional: a senior software engineer at a fintech company, a partner-track attorney at a mid-sized firm, or a physician in private practice. This individual earns $500,000 annually and currently resides in New York City.

The Tax Calculation

Current New York burden:

- Annual income: $500,000

- Effective combined tax rate: 9.5%

- Annual NY State + NYC taxes: $47,500

After moving to Florida:

- Annual income: $500,000

- Florida income tax: $0

- Annual savings: $47,500

- Monthly savings: $3,958

Converting Savings to Mortgage Power

Using standard mortgage calculations at current rates, we can determine how much home this professional can afford using tax savings alone to cover the mortgage payment.

Mortgage assumptions:

- Interest rate: 6.5%

- Term: 30 years fixed

- Rule of thumb: $1,000 monthly payment ≈ $160,000 in loan principal

Calculation:

- Monthly tax savings: $3,958

- Supported loan amount: $3,958 × 160 = $633,280

- With 20% down: Total home price ≈ $791,600

What This Buys in Miami

With approximately $790,000 to spend, this buyer enters Miami’s solid mid-market segment with excellent options:

- Brickell: Modern one- or two-bedroom condos in newer buildings.

- Edgewater: Waterfront or near-waterfront condos in contemporary towers.

- Midtown Miami: Two-bedroom condos in mixed-use developments.

- Coral Gables: Older condo buildings or smaller townhomes.

- Doral: Three-bedroom townhomes or single-family homes.

| Metric | Amount |

|---|---|

| Annual Income | $500,000 |

| NY Effective Tax Rate | 9.5% |

| Annual NY Taxes | $47,500 |

| Annual FL Savings | $47,500 |

| Monthly Savings | $3,958 |

| Supported Loan | $633,280 |

| Home Price (20% down) | $791,600 |

Scenario 2: The $1 Million Income Earner

Our second scenario involves a more senior professional: a finance vice president, a senior partner at a law firm, a successful entrepreneur, or a portfolio manager at a hedge fund. This individual earns $1 million annually.

The Tax Calculation

Current New York burden:

- Annual income: $1,000,000

- Effective combined tax rate: 11.5%

- Annual NY State + NYC taxes: $115,000

After moving to Florida:

- Annual income: $1,000,000

- Florida income tax: $0

- Annual savings: $115,000

- Monthly savings: $9,583

Converting Savings to Mortgage Power

The monthly savings of nearly $9,600 represents substantial purchasing power in the mortgage market.

Calculation:

- Monthly tax savings: $9,583

- Supported loan amount: $9,583 × 160 = $1,533,280

- With 20% down: Total home price ≈ $1,916,600

What This Buys in Miami

At approximately $1.9 million, this buyer accesses Miami’s upper-tier market with impressive options:

- Brickell (High-End): Larger two- or three-bedroom units in premium towers.

- Edgewater Waterfront: Direct bay-front condos.

- Coconut Grove: Condos in boutique luxury buildings or townhomes.

- Coral Gables: Larger single-family homes or luxury townhomes.

- Miami Beach: Select units in Art Deco or mid-century buildings.

- Key Biscayne: Waterfront condos with beach access.

| Metric | Amount |

|---|---|

| Annual Income | $1,000,000 |

| NY Effective Tax Rate | 11.5% |

| Annual NY Taxes | $115,000 |

| Annual FL Savings | $115,000 |

| Monthly Savings | $9,583 |

| Supported Loan | $1,533,280 |

| Home Price (20% down) | $1,916,600 |

Scenario 3: The $2 Million Income Earner

Our final scenario examines a C-suite executive, a successful business founder, or a senior investment professional earning $2 million annually.

The Tax Calculation

Current New York burden:

- Annual income: $2,000,000

- Effective combined tax rate: 13.5%

- Annual NY State + NYC taxes: $270,000

After moving to Florida:

- Annual income: $2,000,000

- Florida income tax: $0

- Annual savings: $270,000

- Monthly savings: $22,500

Converting Savings to Mortgage Power

Monthly tax savings exceeding $22,000 provide access to Miami’s luxury market.

Calculation:

- Monthly tax savings: $22,500

- Supported loan amount: $22,500 × 160 = $3,600,000

- With 20% down: Total home price ≈ $4,500,000

What This Buys in Miami

At $4.5 million, this buyer enters the true luxury segment with exceptional properties:

- Coconut Grove Luxury Towers: Expansive three- or four-bedroom residences.

- Key Biscayne Premium: Beachfront condos with resort-style amenities.

- Brickell Branded Residences: Units in ultra-luxury developments.

- Penthouses: Top-floor units in premium buildings.

- Coral Gables Estates: Substantial single-family homes.

| Metric | Amount |

|---|---|

| Annual Income | $2,000,000 |

| NY Effective Tax Rate | 13.5% |

| Annual NY Taxes | $270,000 |

| Annual FL Savings | $270,000 |

| Monthly Savings | $22,500 |

| Supported Loan | $3,600,000 |

| Home Price (20% down) | $4,500,000 |

Complete Tax Savings Comparison

Here’s a comprehensive view of how moving to Florida impacts purchasing power across all three income levels:

| Income | Effective Tax Rate | Annual NY Tax | Annual Savings in FL | Monthly Savings | Est. Loan Amount | Est. Home Price |

|---|---|---|---|---|---|---|

| $500,000 | 9.5% | $47,500 | $47,500 | $3,958 | $633,000 | $791,000 |

| $1,000,000 | 11.5% | $115,000 | $115,000 | $9,583 | $1,533,000 | $1,916,000 |

| $2,000,000 | 13.5% | $270,000 | $270,000 | $22,500 | $3,600,000 | $4,500,000 |

The progression is striking. As income increases, the tax savings grow disproportionately due to New York’s progressive structure, creating exponentially greater real estate purchasing power in Florida.

Miami Neighborhoods That Match Your Budget

Understanding the tax savings is only half the equation. Knowing where those savings translate into desirable properties completes the picture.

- Under $1 Million ($500k income bracket): Brickell, Edgewater, Coral Gables, and Doral.

- $1-2.5 Million ($1M income bracket): Premium properties in established luxury buildings.

- $2.5-5 Million ($2M income bracket): Branded residences, penthouse units, and waterfront estates.

Each neighborhood offers distinct characteristics. Brickell emphasizes urban energy. Coconut Grove provides village charm. Coral Gables offers Mediterranean elegance. Miami Beach delivers oceanfront lifestyle. Key Biscayne combines island tranquility with easy city access.

Establishing Florida Residency the Right Way

The tax savings discussed throughout this article depend entirely on establishing legitimate Florida residency. This requires more than purchasing property—it demands demonstrating genuine intent to make Florida your permanent home.

The 183-Day Rule

New York considers you a resident if you maintain a permanent place of abode in New York and spend more than 183 days in the state during the tax year. To avoid this, you must spend at least 183 days in Florida (or outside New York).

The Domicile Test

Domicile represents your true, permanent home—the place you intend to return to and remain indefinitely. New York scrutinizes various factors to determine domicile.

Practical Steps for Establishing Florida Residency

- File a Declaration of Domicile with your Florida county clerk.

- Obtain a Florida driver’s license within 30 days.

- Register to vote in Florida and cancel New York voter registration.

- Register vehicles in Florida and update insurance.

- Change your address with banks, brokerage firms, and credit cards.

- File for Florida homestead exemption if applicable.

- Update professional affiliations and licenses where possible.

- Maintain detailed records of days spent in each location.

- File a non-resident return with New York if you have New York-source income.

Working with Professionals

High-income individuals face elevated audit risk when changing residency from New York. Consult with a CPA or tax attorney who specializes in multi-state taxation before making the move. They can review your specific situation and ensure you’re taking all necessary steps to establish and defend your Florida residency.

Property Taxes: New York vs. Florida

The income tax savings dominate the financial calculus of moving to Florida, but property taxes deserve consideration in any complete analysis.

The Bottom Line

Yes, Florida property taxes generally exceed New York City property taxes for comparable home values. However, this difference rarely exceeds $10,000 annually—a small fraction of the income tax savings. For our $1 million earner saving $115,000 annually in income taxes, paying an additional $10,000 in property taxes still yields net savings of $105,000.

People Also Ask

Can moving to Florida really save enough to cover a mortgage?

Yes, for high-income earners. Someone making $1 million annually saves approximately $115,000 in state and local income taxes by moving to Florida, which translates to $9,583 monthly—enough to support a mortgage on a $1.9 million home.

How much does a high earner pay in NYC taxes?

A professional earning $500,000 pays approximately $47,500 annually in combined New York State and New York City income taxes (9.5% effective rate). At $1 million income, the burden reaches $115,000 (11.5%). At $2 million, it climbs to $270,000 (13.5%).

Are Florida property taxes higher than New York?

Generally yes, but the difference is modest compared to income tax savings. Florida property taxes on a $1 million home run approximately $20,000-25,000 annually, while comparable New York City property taxes range from $10,000-15,000.

Will New York audit me if I move?

New York does audit high-income individuals who change residency. Maintaining detailed records, spending substantial time in Florida, and severing New York ties reduces audit risk. Work with a tax professional.

Does moving to Florida reduce overall cost of living?

The transformative savings come from taxes, not general cost of living. The income tax elimination provides the primary financial benefit for high earners.

Conclusion: Your Path Forward

The mathematics are clear: moving to Florida creates genuine, substantial financial benefits for high-income professionals currently residing in New York City. The elimination of state and local income taxes produces monthly savings that directly translate into mortgage-buying power.

The question isn’t whether moving to Florida saves money—it demonstrably does. The question is whether the lifestyle, business opportunities, and personal preferences align with your goals beyond the financial calculus.

Let’s Find Your Perfect Home in Florida

Contact me today for a private consultation on how your New York tax savings could translate into a Miami home that matches your lifestyle and financial goals.